(Doc. T93-122, as amended)

I. Introduction

These Administrative Standards (“Standards”) are intended to assist in the implementation of the University of Massachusetts’ (“University”) Capital Planning, Land, and Facilities Use Policy (T93-122) (“Policy”). The Policy provides a framework within which the University develops and reviews Campus master plans, the University’s five-year capital plan, and the review and approval of capital projects. It includes other related topics such as capital renewal, ongoing maintenance, and the disposition, acquisition, and use of real estate.

II. Definitions

- Alternative Financing and Delivery – A contractual arrangement between a public entity and a private sector developer whereby a range of project risks and responsibilities can be transferred to the private sector developer.

- Approved Capital Project List – A list of capital projects, as defined below, which is reviewed quarterly and approved by the University President or the Board of Trustees.

- Campus – Amherst, Boston, Dartmouth, Lowell, Chan Medical School.

- Capital Project – Construction, capital equipment for construction, lease (whether as lessee or lessor) of land and/or facilities, land or real property acquisition or disposition requiring review by the University President or the Board of Trustees.

- Capital Project Review – Prior to Vote 2 and for all Capital Projects with a Total Value of $2 million or greater, a review to evaluate the scope and cost of each Capital Project to ensure rationality and feasibility and to ensure compliance and avoid unforeseen cost increases. For all Capital Projects managed by the UMass Building Authority (“UMBA”), the Capital Project Review is conducted by UMBA; for all Capital Projects not managed by UMBA, the Capital Project Review is conducted by the Campus in consultation with the President’s Office.

- Capital Projects Screening – High-level screening process performed for each Capital Project prior to receiving preliminary approval in order to determine the suitability of alternative delivery. This checklist is included in Appendix B to these Standards.

- Catch Up Spending – Capital Projects funded by reserves, bond proceeds, and/or State resources (e.g., typically bond bill funds) for the purposes of retiring the deferred maintenance backlog.

- Five-Year Capital Plan (“Capital Plan”) – The Capital Plan contains priority Capital Projects that each Campus intends to start over the five-year planning period. The Capital Plan is updated biennially and is informed by each Campus’ Master Plan (as defined in Article III, Section A.1 below). Capital Projects incorporated into a Campus’ Capital Plan must be reviewed and approved by the Board of Trustees or the University President before a Campus may move forward with a project.

- Keep Up Spending – Recurring operating budget or capitalized expenses for the following types of projects:

- Small Operating Projects – Projects with a cost up to $20,000, which include, but are not limited to, carpet replacement, hot water heater replacement, LED conversions, small bathroom renovation, air handling unit replacement, reconfiguration of vacated space, etc.;

- Preventive and Proactive Maintenance – Systematic and proactive projects adding value to the operating conditions of equipment, which include, but are not limited to, inspections, testing, lube/oil, filter changes, belt changes, elevator maintenance, fire alarm maintenance, fire suppression system inspection, roof inspections, mechanical/electrical inspection, and building management system inspections; and

- Recurring Projects – Projects not bonded and funded through the annual operating budget.

- Project Phases – There are nine (9) pre-defined Capital Project phases ranging from conceptual design to completion. Each Campus will categorize and track Capital Projects using the following phases:

- Conceptual

- Feasibility Report

- Owner’s Project Manager / Designer Procurement

- Study / Schematic Design

- Design

- Final Design / Early Construction Packages

- Construction

- Substantial Completion

- Complete

- Construction Complete

- Financially Complete

- Total Value (referred to as “Total Cost” in the Policy) – For purposes of Capital Projects subject to the Policy, “total value” includes (i) all estimated project costs (construction costs and soft costs) and costs incurred or expenditures made, and/or (ii) all anticipated proceeds received or revenue earned.

- UMBA Real Estate – Real property owned and/or financed by UMBA for the use and benefit of the University.University Real Estate – Real property owned by the Commonwealth of Massachusetts and held and managed by the University Board of Trustees for the use and benefit of the University. For the purposes of the Policy and these Standards, University Real Estate does not include UMBA Real Estate.

III. Standards Statement

A. Campus Land and Facilities Use Master Plans; Capital Planning and Project Review and Approval

- Development of the Land and Facilities Use Master Plan – Each Campus shall prepare and maintain a land and facilities use master plan(s) (“Campus Master Plan”), which shall include, at a minimum:

- Information about the Campus’ mission and goals.

- An inventory and description of existing land and facilities, including a description of the possible new or revised use of existing land and facilities.

- In assessing proposals for a change in the use of existing facilities and/or land, Campuses should consider the following:

- The short-and long-term cost implications must be beneficial to the University;

- The potential financial, legal and reputational risks; and

- Compliance with private use requirements as set forth in Article III.G of these Standards.

- In assessing proposals for a change in the use of existing facilities and/or land, Campuses should consider the following:

- Projections of future land and facilities’ needs, consistent with the Campus academic vision, strategic plan, long-range enrollment plan, or other guiding strategic plans.

- The assumptions and criteria used to identify the needs of the Campus, including the expected impact of capital investment (if any) on Campus key financial ratios.

- The plan(s) shall be consistent with State requirements for facilities and land use master plans.

- The Campus Master Plan(s) shall be consistent with the Capital Plan and other capital planning and land use decisions.

- The Campus Master Plan(s) shall be submitted and reviewed by the University President. The Campus Master Plan(s) shall be updated on a periodic or rolling basis, including when substantial changes to the Campus’ mission statement or strategic goals have taken place.

- Development of the Capital Plan

Frequency: Biennially

The Capital Plan shall include, but may not be limited to the following:- A prioritized list of all Campus Capital Projects over $2 million in total project cost that are planned to be initiated over the next five years, and in the aggregate, are projected to be affordable under currently forecast financial conditions.

- A statement on how each Capital Project supports the mission and goals of the Campus.

- A statement describing how each Capital Project addresses the deferred maintenance needs of the Campus.

- A projection of funding sources that will be utilized to pay for the design and construction of each project, including:

- University local funds (operating, plant, or other funds).

- External funds including private fundraising and grants.

- Revenue projected to be generated by virtue of the development of the project.

- State appropriations – G.O. funds or supplemental funds.

- Alternative financing through third parties and/or other partnerships.

- The Capital Plan shall be updated biennially and requires the approval of the University President and the Board of Trustees.

- The Board of Trustees vote to approve the Capital Plan does not constitute approval of an individual Capital Project and all future Capital Projects are required to follow the capital approval process set forth in Section III.A.3.

- Capital Project Review and Approval Process

Frequency: Quarterly

Before a Campus can proceed with a Capital Project, it must receive the requisite approval by the University President and/or the Board of Trustees, as follows:- Any Capital Project with a total value between $2 million and $10 million may proceed with the approval of the University President.

- Any Capital Project with a total value greater than $10 million requires the approval of the Board of Trustees.

- Any Capital Project with a total value greater than $2 million that requires any amount of University borrowing requires the approval of the Board of Trustees.

- Capital Projects that have received the Second Vote that have an increase in cost of 10% or more will require an additional approval from the Board of Trustees.

- The status of all Capital Projects will be tracked by the President’s Office and reported to the Board of Trustees on a quarterly basis.

Project Screening and Approval Process

Frequency: On-going

There are two paths a Capital Project can take to be approved. To proceed with any phase of design or construction, the following process must be followed in order to obtain the required votes by the President or Board of Trustees for Traditional Projects, or by the Board of Trustees for Alternative Projects.INSERT TABLE OF APPROVAL PROCESS HERE

- Quarterly Reporting to the Board

Frequency: Quarterly

- The status of all Capital Projects will be tracked and reported to the Board of Trustees on a quarterly basis.

- In order to facilitate quarterly reporting to the University President and the Board of Trustees, Campuses will use a Capital Project database to update project information, monitor approvals and request new projects. Instructions will be sent out by the President’s Office each quarter and will be updated as needed. It is each Campus’ responsibility to ensure accuracy and review each field in the Capital Project database to make sure the information is updated and accurate.

- Changes to Project Costs

Frequency: Quarterly

As part of the quarterly reporting to the Board of Trustees all project costs will be provided for each project on the list. Capital Projects that have received the Second Vote that have an increase in cost of 10% or more will require an additional approval from the Board of Trustees.

Before the Board of Trustees votes on a revised project cost, the following must be provided to the Board of Trustees:- A detailed description of the reason for the change in cost;

- A Campus must identify funding for the additional amount needed;

- If the additional amount is being borrowed, evidence that the debt affordability analysis complies with the University debt policy;

- UMBA’s review and approval on the revised project cost estimate; and

- For State projects, evidence that the Division of Capital Management and Maintenance (DCAMM) reflects the increased cost in its project list and EOAF has included the change in its latest capital plan.

- Transfers between UMBA and the University

Frequency: As needed

Any cash transfer of $5M or greater to UMBA for a Capital Project will require approval by the Senior Vice President of A&F and Treasurer. The Vice Chancellor of A&F from the requesting Campus will submit a formal request to the Senior Vice President detailing the need for the transfer. Any approved transfer must be reflected appropriately in the capital plan funding sources. - Traditional Project Spending Prior to Vote 2

Frequency: As needed

Issuing commercial paper or long-term bonds may not occur for a Capital Project until it has received the Vote 2 from the Board of Trustees and approval from the Executive Office of A&F. Therefore, no spending on Capital Projects in Vote 1 status may come from borrowed funding sources.

B. Funding Deferred Maintenance: "Keep Up" and "Catch Up" Maintenance of Facilities

- Establishing Spending Targets

- Annually, the President’s Office will issue instructions as part of the annual budget and 5-year forecast exercises detailing the annual “Keep Up” target for each Campus. Targets should be based on the capital investments necessary to meet the facility lifecycle cost analysis, which shall be performed annually by a third party. Annual investments should grow in accordance with guidance issued periodically by the President’s Office in order to achieve the annual Keep Up Spending target and prevent deferred maintenance backlog growth.

- Spending amounts to address “Catch Up” needs should be set with the goal of significantly reducing the University’s deferred maintenance backlog over an established time period. The President’s Office will annually track and report on progress toward meeting the Catch Up goal.

- Reporting and Monitoring of Spending. All plant funds or capital project IDs will require a designation of Keep Up, Catch Up, or exclude. Campuses will maintain these designations for existing projects and any newly added projects in Peoplesoft. The President’s Office will maintain a Deferred Maintenance Spending Dashboard which will summarize Keep Up and Catch Up spending using these designations. Spending progress in relation to targets will be presented to the Board of Trustees in each quarterly capital report.

- Spending Requirements. To ensure that adequate resources are available to meet the deferred maintenance needs of each Campus as established though the Keep Up and Catch Up requirements noted above, the following funds shall be budgeted and/or accumulated:

- For any new building, one and one half percent (1.5%) of its replacement value shall be transferred annually to the Unexpended Plant and Facility reserve to help fund the future deferred maintenance needs of new buildings. Campuses may obtain an exemption from this reserve requirement by submitting a request to the University President. Exemption requests will be evaluated on a case-by-case basis and approved by the University President or his/her designee.

- The replacement value will be determined by the value used to record it on the books and the annual contribution to reserves will begin at the time the building is placed in service and the depreciation of the asset is recorded.

- Each Campus must fully fund depreciation:

- Full funding of depreciation is expected to support, through recurring resources, each Campus’ annual principal debt payments and additional capital investments sufficient to meet the Keep Up target as defined in Section II of these Standards.

- In the event that fully funding depreciation does not allow a Campus to meet its Keep Up target, after accounting for its annual principal debt payments, the Campus must develop a plan to be approved by the University President to ensure that the Keep Up target is funded from operating dollars.

- Annually, each Campus must include adequate funding in the annual operating budget for operational and maintenance expenses of the Campus facilities based on industry best practices.

- For any new building, one and one half percent (1.5%) of its replacement value shall be transferred annually to the Unexpended Plant and Facility reserve to help fund the future deferred maintenance needs of new buildings. Campuses may obtain an exemption from this reserve requirement by submitting a request to the University President. Exemption requests will be evaluated on a case-by-case basis and approved by the University President or his/her designee.

C. Disposition & Acquisition of University Real Estate

- These Standards are intended to implement those portions of the Policy concerning the disposition and acquisition of University Real Estate. These Standards also are intended to govern Campus requests for the acquisition and disposition of UMBA Real Estate utilized by a campus. The University is responsible for the management and maintenance of all University Real Estate and, pursuant to the Second Amended and Restated Master Contract for Financial Assistance, Management and Services, has agreed to manage and maintain UMBA Real Estate. In the case of any inconsistency between the Policy and these Standards, the Policy shall govern. All capitalized terms used in these Standards shall have the same meanings as set forth in the Policy.

- Disposition. For the purposes of the Policy and these Standards, a “disposition” is a conveyance of University Real Estate or an ownership interest therein from the University to another party or a request of a Campus for a conveyance of UMBA Real Estate being utilized by the campus. Disposition of University Real Estate may occur by sale, gift, exchange, or other grant or transfer. Except as otherwise set forth herein, disposition of University Real Estate shall require prior consultation and approval by DCAMM and/or the Legislature and the Governor. In order to allow for adequate review and analysis, Campus proposals for all dispositions of University Real Estate and Campus requests for the disposition of UMBA Real Estate being utilized by the campus must be presented to the Board of Trustees for informational purposes at one meeting and presented at a later meeting for the Board of Trustees’ approval. Such proposals must contain particular findings as to why the real estate no longer serves the current and future needs of the University as well as a description of the process to be utilized by the Campus to complete the disposition and the anticipated proceeds to be earned from the transaction. Any disposition of University Real Estate by a Campus must be in the best interest of the University and consistent with the Campus Master Plan.

- Disposition of University Real Estate to UMBA shall not require consultation and approval by DCAMM and/or the Legislature and the Governor.

- Acquisition. For the purposes of the Policy and these Standards, an “acquisition” is a conveyance of real estate or an ownership interest therein to the University, or a Campus request to UMBA for the acquisition of real property on behalf of a campus. Acquisition of real estate may occur by gift, purchase, exchange, or other grant or transfer. Prior to the acquisition of real estate by or on behalf of a Campus, the Campus must conduct a due diligence review, provided, however, any acquisition of real property by UMBA on behalf of a Campus shall be pursuant to the applicable UMBA legislation and/or policies. Such review shall include (i) the anticipated cost based on recent appraisals, assessments and other available information, (ii) an environmental investigation identifying any concerns and/or confirming the environmental condition, (iii) an evaluation of all improvements, and (iv) an appropriate title search confirming the title for the property is in acceptable condition (i.e. no unduly burdensome encumbrances or restrictions). All acquisitions of real estate by the University must be in the best interests of the University and consistent with the Campus Master Plan. Any proposed acquisition of real estate by or on behalf of a Campus with (i) a total estimated cost greater than $10 million; or (ii) a total estimated cost greater than $2 million that also requires University borrowing, must be approved by the Board of Trustees.

D. Agreements on the Use of Real Estate

- These Standards are intended to implement those portions of the Policy concerning the use of real estate by the University. These Standards shall apply to the negotiation and execution of leases, licenses, and other agreements regarding the use of University Real Estate and the University’s use of real estate owned by other parties.

- Capital Projects. Any Capital Project that requires the execution of an agreement for the use of real estate (i) owned by the University or (ii) owned by any other party shall be subject to the approval requirements set forth in Article III, Section A(3) of these Standards based on the total estimated value of the project. Any agreement for the use of real estate that does not meet the threshold for approval as a Capital Project shall be subject to the following requirements:

- Agreements for the Use of University Real Estate. The University may, from time to time, enter into agreements to permit third parties to use University Real Estate for research and academic purposes or other uses that are consistent with the University’s mission. Any request for a third party to use UMBA Real Estate is subject to UMBA’s approval and must be approved by UMBA and its bond counsel in its sole discretion. Any proposed use of University Real Estate by any entity or person through a lease, license, or other agreement with a term of less than ten (10) years, including any optional extensions or renewals, may be approved by the Campus or President’s Office. Any Campus seeking to lease, license, or otherwise allow for the use of University Real Estate for a term of ten (10) years or more, including any optional extensions or renewals, or any Campus request for a third party to use UMBA Real Estate for a term of ten (10) years or more, must obtain the final review and approval of the University President. The guidelines set forth below in paragraph 7 of this section D explain the process and criteria required to obtain the University President’s approval of such agreements. The University President may request additional information regarding such agreements as needed. Whenever practicable or required by law, Campuses should use a public process to solicit competitive offers when making University Real Estate available for use by other parties to assure best value for the University. Any request for a third party to use UMBA Real Estate is subject to UMBA’s approval in its sole discretion.

- Easements or Other Agreements with Public Utilities, Municipalities, and Service Providers. When deemed beneficial to the University, a Campus may grant easements or enter into agreements with public utilities, municipalities, service providers, or other parties to allow for the limited use of University Real Estate in order to facilitate the delivery of utilities or services to the Campus or to abutting properties. In certain circumstances, the University may also enter into agreements not to perform, exercise, use, or conduct a lawful activity on a portion of University Real Estate for the benefit of a third party, however such agreements shall be treated the same as any other grant of use of University Real Estate and shall be subject to the same requirements for approval as set forth above in paragraph 3 of this section D. Any proposed easement or any other limited use as described in this paragraph involving UMBA Real Estate is subject to UMBA’s approval in its sole discretion.

- Agreements for the University’s Use of Real Estate Owned by Other Parties. Any proposed use by the University of real estate owned by another party (excluding UMBA) through a lease, license, or other agreement with a term of less than ten (10) years, including any optional extensions or renewals, may be approved by the Campus or President’s Office. Any Campus seeking to lease, license, or otherwise provide for the University’s use of real estate owned by another party (excluding UMBA) for a term of ten (10) years or more, including any optional extensions or renewals, must obtain the final review and approval of the University President. The guidelines set forth below in paragraph 7 of this section D explain the process and criteria required to obtain the University President’s approval of such agreements. The University President may request additional information regarding such transactions as needed. Whenever practicable or required by law, Campuses should use a public process to solicit competitive offers when seeking to lease or license real estate for use by the University.

- Extensions of Agreements. If a Campus intends to extend the term of any lease, license or other agreement concerning the use of University Real Estate and/or the University’s use of real estate owned by other parties (excluding real property owned by UMBA) to a term of ten (10) years or more, and such lease, license, or agreement was not subject to the University President’s approval upon initial execution, the Campus must obtain the final review and approval of such extension by the University President.

- Submission of Agreements for Presidential Approval. Any proposed real estate transaction by a Campus requiring the approval of the University President pursuant to paragraphs 2-6 of this section D shall be submitted for the University President’s review, with copy to the Senior Vice President for Administration & Finance, accompanied by a memorandum from the Chancellor or his/her designee describing the proposed transaction and the reason(s) for entering into the transaction. Such memorandum should include, but not be limited to, the following information: (i) a description (including improvements) and location of the property; (ii) the term of the lease or agreement, including any extensions or renewals; (iii) the rent and other anticipated additional charges or costs if the University is lessee, including build-out or construction expenses, furnishings, and utilities; (iv) the anticipated revenue if the University is the lessor, based on comparable leased properties or other available information; and (v) memorandum from Office of the General Counsel confirming review and legal acceptability of the proposed documents for execution. In the event a Campus enters into a letter of intent to pursue a real estate transaction that will require the approval of the President pursuant to these Standards, the Campus shall provide notice of the execution of such letter of intent to the President’s Office.

- Fair Market Value. Any proposed real estate conveyance to or by a Campus subject to these Standards shall be at fair market values, supported by a comparable market analysis of rents or other applicable rates. Any proposed real estate transaction by a Campus at other than fair market value shall include a written justification explaining why such transaction is in the best interests of the University.

E. Other Undefined Projects

Projects not defined in these Standards or which otherwise are not clearly categorized into one of the sections above should be submitted for consideration to the Senior Vice President of A&F and Treasurer by the requesting Campus. The Senior Vice President of A&F and Treasurer will consult with UMBA and Office of the General Counsel to determine the approval process for the project. Whenever possible, projects will be assigned to the most appropriate existing approval process.

F. Review by Office of the General Counsel

- Any interpretation or questions related to Sections C-E herein shall be submitted for legal review to the Office of the General Counsel.

- Transaction documents contemplated under Sections C-E shall constitute Real Property Agreements, as defined in the Procurement Policy and associated Administrative Standards for the Procurement Policy (Doc. T92-031) (“Procurement Policy and Standards”). The General Counsel, or an attorney in the Office of the General Counsel as the General Counsel may determine, shall review and determine legal acceptability of any Real Property Agreement prior to execution as set forth in the Procurement Policy and Standards. Review by the Office of the General Counsel under this Policy and the Procurement Policy and Standards is in addition to any other internal approvals that may be required under other University and any other notices to the Office of the General Counsel contemplated herein.

- No provision in these standards shall be construed as to limit UMBA’s powers under its Enabling Act.

G. Private Business Use

- Any facilities of the Campuses that are purchased, constructed, renovated, rehabilitated, improved or otherwise funded by use of funds from a tax-exempt bond issue are subject to limitations on “Private Business Use”, as defined below, and as further described in the federal tax law. Excessive Private Business Use of facilities financed with tax-exempt bonds may cause the interest on the tax-exempt bonds to become taxable to the holder of the bonds.

- “Private Business Use” (“PBU”) is defined as direct or indirect use of the tax-exempt bond financed facilities in any activity carried on by any party other than a “Qualified User.” As used herein a Qualified User is a state or local governmental unit or, in certain circumstances, a nonprofit, charitable organization described in Section 501(c)(3) of the Internal Revenue Code using facilities in furtherance of its tax-exempt purpose. The federal government is not a Qualified User for the purposes of Private Business Use.

- Any intended Private Business Use by a party other than a Qualified User of University Real Estate that is purchased, constructed, renovated, rehabilitated, improved or otherwise funded by use of funds from a tax-exempt bonds user must be reviewed and monitored by UMBA in consultation with the University.

- The University shall comply with all applicable Private Business Use restrictions, including, but not limited to, any restrictions set forth in policies issued by UMBA.

IV. Financial Ratios & Benchmarks

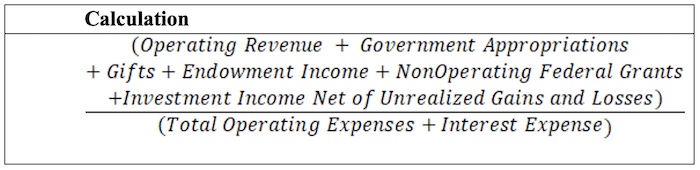

- Operating Margin – indicates whether total operating activities resulted in either a surplus or deficit as a percentage of the budget.

Calculation: Begin fraction, begin numerator, open paranthesis, total: Operating Revenue plus Government Appropriations plus Gifts plus Endowment Income plus NonOperating Federal Grants plus Investment Income Net of Unrealized Gains and Losses, close parenthesis, end numerator, open denominator, open parentheses, total: Operating Expenses plus Interest Expenses, close paranthesis, end denominator, end fraction Debt Burden Ratio – compares the relative cost of borrowing to overall expenditures.

Calculation: Begin fraction, begin numerator, Debt Service (P&I), end numerator, begin denominator, open paranthesis, total: Operating Expenses plus Interest Expenses, close paranthesis, end denominator, end fraction.

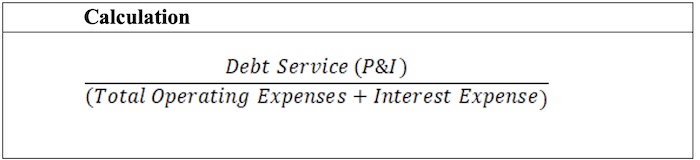

- Debt Coverage Ratio – measures the ability to make debt service payments from annual operations.

Calculation*: Begin fraction, begin numerator, total: open paranthesis, total revenues minus total expenses, close paranthesis, plus Depreciation, plus Interest, plus Large Noncash Expenses, end numerator, begin denominator, Debt Service (P&I), end denominator, end fraction.

*Noncash expenses include pension expense and OPEB expense

V. Related Policies and Processes

The Policy and these Standards should be reviewed in consultation with:

- Debt Policy (T09-050)

- University Reserve Policy (T18-026)

- Procurement Policy (T92-031, Appendix A)

- Annual 5-year Financial Forecast

- Annual Operating Budget

- UMBA Policy and Procedures for the Purchase and Sale of Real Estate and all other relevant policies and procedures.